Statement of Counseling Services

Please read the following statement of counseling services carefully to understand our procedures if you have any question please contact us:

1. I understand the program will provide confidential, comprehensive personal money management interviews should I choose to pursue a one-on-one financial counseling arrangement. In addition to general financial counseling, Goodwill Industries of North Central Wisconsin, Inc. (Goodwill NCW) also provides counseling in bankruptcy and educational workshops. Clients are not obligated to receive or purchase any other services offered by Goodwill NCW in order to receive counseling of any type, including but not limited to budget, or bankruptcy counseling.

2. I understand that a certified consumer credit counselor or qualified consumer credit counselor will conduct the interview. All action plans not conducted by a certified consumer credit counselor will be reviewed by a certified credit counselor. Our counselors are trained and certified in accordance with the National Association of Certified Credit Counselors. A qualified consumer credit counselor has been trained but has not, as yet passed all of the

required tests.

3. I understand if I am dissatisfied, I can utilize the Grievance Procedure Process.

4. I understand that financial counseling is offered without regard to a debtor’s ability to pay. Bankruptcy counseling fees will be waived if your income is less than 150 percent of the poverty guidelines updated periodically in the Federal Register by the U.S. Department of Health and Human Services under the authority of 42 U.S.C. 9902(2), as adjusted from time to time, for a household or family of the size involved in the fee determination. I understand that financial support for the agency comes from various funders.

5. I understand that the decisions I make regarding my financial concerns are ultimately the result of my own choices. Therefore, I agree to hold the agency, its employees and volunteers harmless from any claim, suit, action or demand of my creditors, myself or any other person resulting from advice or counseling. Nothing herein shall apply to actions or claims under the provisions of the United States Bankruptcy Code, 11 U.S.C 101 et seq.

6. Should I choose to seek one-on-one counseling, I understand that, in that process, I will be given a written assessment outlining a suggested client action plan which will be based on the following options:

a. I may choose to handle financial concerns on my own.

b. I may choose to be referred to a Debt Management Program (DMP). A DMP serves a dual role of helping me repay my debts and helping creditors to receive the money owed to them.

• My participation in a debt repayment program may change information which is already on my credit report. If my credit report reflects that I have paid creditors as agreed in the past, a Debt Repayment Plan could have a negative impact on a creditworthiness decision by a potential creditor, landlord, or employer in the future.

• In addition, creditors may report that I am on a Debt Management Program and am not paying as originally agreed although they have accepted the reduced payment.

• I understand the agency has no responsibility or obligation for any past, present, or future credit rating I receive.

c. I should also be aware that debts to creditors I repay through the plan may be able to be discharged through bankruptcy. Counselors may answer questions about bankruptcy but cannot provide legal advice.

d. I may be referred to other services of the organization or another agency or agencies as appropriate that may be able to assist with particular problems that have been identified.

7. I understand that receipt of financial counseling services does not automatically guarantee a referral to a Debt Management Program.

8. I understand that at some time in the future, my information may be used for confidential research and/or a neutral third party may contact me to request an evaluation of the program’s services.

Pre-Bankruptcy Counseling Disclosure

People who are considering filing for bankruptcy are required to receive “counseling” before filing. Goodwill Industries of North Central Wisconsin, Inc. (Goodwill NCW, We or Us) will do a budget analysis examining your financial situation, discuss factors that may be causing problems, and explore options for developing a reasonable plan for dealing with them. We will provide you with information about bankruptcy, its process and possible consequences.

1. We charge a fee of $50 per person. This fee will be waived if your current income is less than 150 percent of the poverty guidelines updated periodically in the Federal Register by the U.S. Department of Health and Human Services under the authority of 42 U.S.C. 9902(2), as adjusted from time to time, for a household or family of the size involved in the fee determination. Please ask us if you have questions about these income levels.

2. Interpreters provided upon request for non-English speakers and the hearing impaired at no cost.

3. There is no additional fee associated with generation of the certificate. No one is turned away if they cannot afford to pay.

4. This agency receives financial support from grants from various funders, including the United Way.

5. The consumer credit counselor conducting or supervising this session has been trained and certified in accordance with the National Association of Certified Credit Counselors (NACCC) standards, and while he/she has expertise in helping those with financial problems, he/she cannot provide you with legal advice. In fact, this session is designed to provide you with information and alternatives; it is not intended to take the place of a consultation with an attorney to explore your legal rights and options.

6. We will discuss any potential impacts on credit reports of all alternatives that we discuss with you. The purpose of this session is to provide you with information so that you may chose the option that you think is best. If you decide to declare bankruptcy, it will remain on your credit report for up to 10 years. Budget and credit counseling do not produce a negative impact on credit scores. If you enroll in a Debt Management Program, a notation may appear on your report that you are making payments through a third party and that the account is closed. That notation is at the discretion of the lender. A consumer’s score is not negatively affected simply by enrolling in a DMP. If you should decide to enter into a DMP (which will be explained in the course of this session) you will be referred to another agency who handles DMPs.

7. We do not pay or receive referral fees for the referral of clients.

8. We will send a certificate to the client, upon completion of credit counseling services, no later than one business day after completion of counseling, and shall issue certificates only in the form approved by the United States Trustee and only from the Certificate Generating System maintained by the United States Trustee.

9. You have the opportunity to negotiate an alternative payment schedule with regard to each consumer debt. We will discuss alternatives to bankruptcy, including the option to negotiate an alternative payment arrangement with your creditors.

10. To assist you, it is essential that you provide us with information that is as accurate and complete as possible. For that reason, We may ask you to authorize Us to access your credit history. Rest assured that the information concerning your financial condition and status that you provide during this session is strictly confidential. Such information would include, but is not limited to, income, debts, credit accounts, earnings, assets, and employment data. We will not disclose any such information that you provide orally or in writing to anyone, except as authorized by you in writing or as required by law, such as in response to a subpoena. We may disclose client information to the United States Trustee in connection with the oversight of the agency, or during the investigation of complaints, during on-site visits, or during quality of service reviews. We may compile data and aggregate information that you give us, but this information will not be disclosed in any manner that would personally identify you. This agency will not disclose or provide any information about this session to a credit reporting agency.

11. The United States Trustee has reviewed only the agency’s debtor education and credit counseling services and has neither reviewed nor approved any other services the agency provides to clients.

12. The certificate is valid for up to 180 days from date of completion of counseling. You must complete counseling services to receive a certificate.

What does Goodwill Industries of North Central Wisconsin (Goodwill NCW) do with Your Personal Information?

Why Do We Collect Information?

Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do.

What Types of Information?

The types of information we collect and share depends on the product or service you have with us. This information can include:

• Social Security Number

• Income

• Assets

• Debt History

• Aggregate Case File Information

• Information Needed by Creditors

When you are no longer our customer, we continue to share your information as described in this notice.

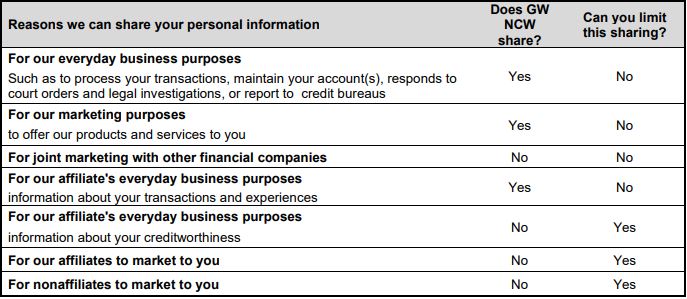

How are we Sharing the Information?

All financial companies need to share customers’ personal information to run their everyday business. In the provided chart, we list the reasons financial companies can share their customers’ personal information; the reasons Goodwill NCW chooses to share; and whether you can limit this sharing.

Have Questions?

Give us a call at 800-366-8161

How do we Protect Your Information?

To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguard and secured files and buildings.

How do we Collect Your Information?

We collect your personal information when you:

• Provide Information to us:

- Verbally

- Through Initial Intake

- Documents you shared

- Income Statement

• Authorize us to pull your credit report

• We also collect information from others, such as credit bureaus and creditors

Why Can’t I Limit the Sharing?

Federal law gives you the right to limit only:

• Sharing for affiliates everyday business purposes – information about your creditworthiness

• Affiliates from using your information to market to you

• Sharing for nonaffiliates to market to you

State laws and individual companies may give you additional rights to limit sharing.

Definitions

Affiliates: Companies related by common ownership or control. They can be

financial and non-financial companies.

Nonaffiliates: Companies not related by common ownership or control. They can be

financial and non-financial companies.

• Financial support for agency comes from various funders who can review and monitor program for compliance and follow-up with clients related to program evaluation.

Joint Marketing: A formal agreement between nonaffiliated financial companies that

together market financial products or services to you.

By clicking the button below, you acknowledge that you understand the disclosures made above.